TPG RE Finance Trust (TRTX)·Q4 2025 Earnings Summary

TPG RE Finance Trust Q4 2025: Distributable Earnings Match Dividend as Originations Surge 25%

February 17, 2026 · by Fintool AI Agent

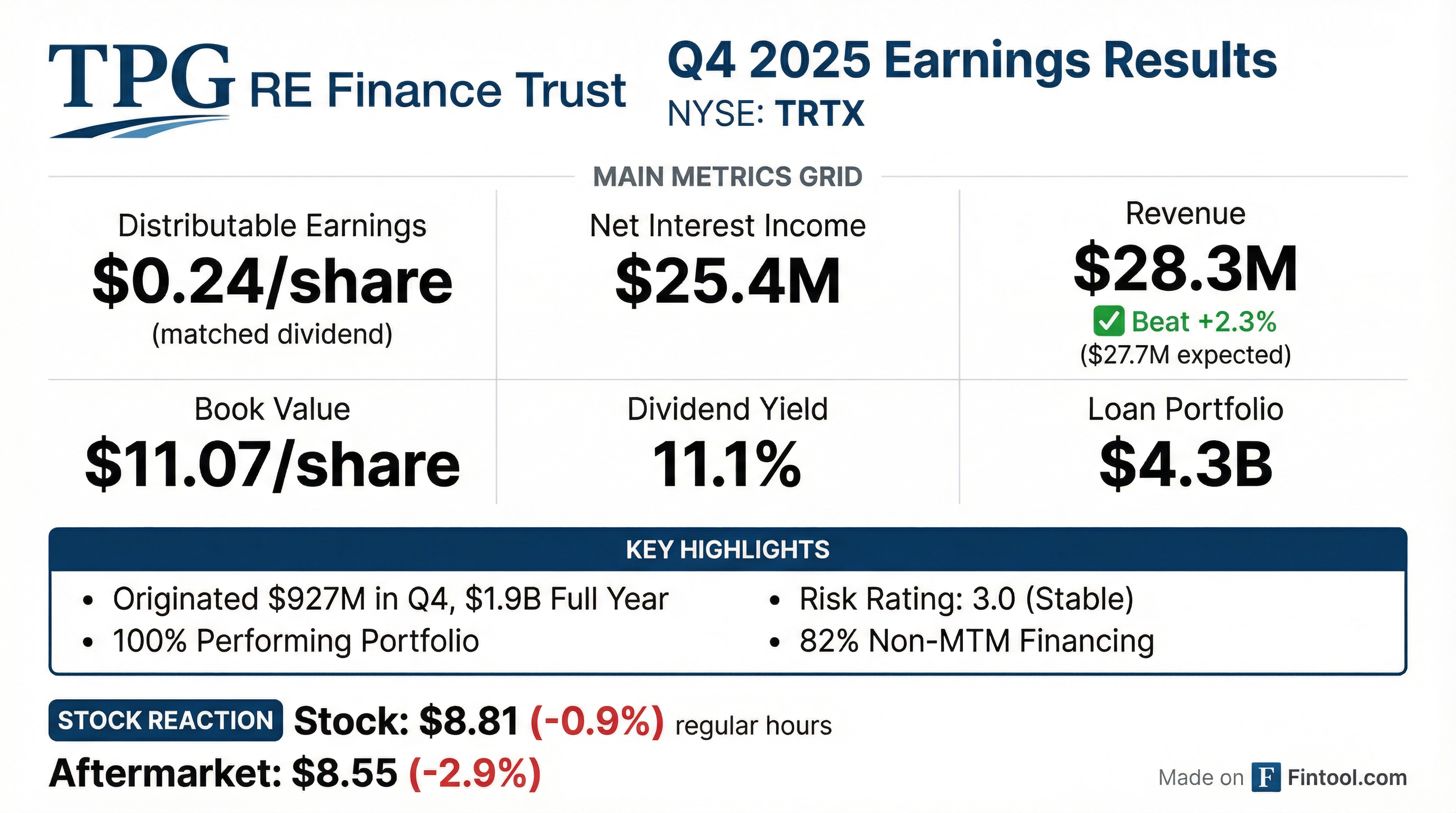

TPG RE Finance Trust (NYSE: TRTX) delivered Q4 2025 results that demonstrated the mortgage REIT's ability to cover its dividend while scaling originations. Distributable earnings came in at $0.24 per share, exactly matching the quarterly dividend, while the company originated a record $927 million in new loans during the quarter.

CEO Doug Bouquard highlighted the balance sheet's velocity: "During 2025, we originated $1.9 billion of total loan commitments, out-earned our common stock dividend, and maintained a 100% performing loan portfolio."

Did TRTX Beat Earnings?

Mixed results — revenue beat while earnings per share narrowly missed:

The GAAP net income was minimal at $0.2 million due to $11.3 million in credit loss expense provisions, which increased the CECL reserve from $66.1M to $77.4M. However, distributable earnings — the key metric for REIT dividend coverage — remained solid at $18.5 million.

What Changed From Last Quarter?

Loan portfolio grew 13% sequentially while risk metrics held steady:

The decline in book value from $11.25 to $11.07 was driven by a combination of factors: credit loss expense ($0.14/share), dividend payments ($0.24/share), offset partially by stock compensation ($0.06/share).

Leverage increased as the company deployed capital into new originations, with the debt-to-equity ratio moving from 2.64x to 3.02x — still well within the 4.25x covenant limit.

What's the Loan Portfolio Mix?

Multifamily dominates at 53% of commitments, with industrial growing the fastest:

The 284% increase in industrial exposure and 40% reduction in office exposure reflects deliberate portfolio repositioning away from challenged property types.

Q4 2025 Origination Activity

$927 million in new loans across nine first mortgages:

Loan repayments totaled $378 million in Q4, with property mix of 56.5% multifamily, 34.5% office, and 9.0% hotel.

How Did the Stock React?

Down modestly in regular trading with further aftermarket weakness:

The stock trades at a 20% discount to book value ($8.81 vs $11.07 book), reflecting broader mortgage REIT sector concerns about office exposure and interest rate volatility. The 11.1% dividend yield suggests the market is pricing in some dividend risk, though management's track record of covering the payout may ease those concerns.

Full Year 2025 Highlights

The company out-earned its dividend by $0.01/share in 2025, with distributable earnings of $0.97 vs dividends of $0.96. Share repurchases added $0.13 to book value per share during the year.

Capital Structure & Liquidity

82% non-mark-to-market financing provides stability:

In Q4, the company issued TRTX 2025-FL7, a $1.1 billion CRE CLO with $957 million of investment-grade bonds at Term SOFR + 1.67% and an 87% advance rate.

Available liquidity of $143 million includes:

- $72.6M cash available for investment (net of $15M covenant reserve)

- $51.4M undrawn capacity on credit facilities

- $4.0M CLO reinvestment proceeds

What Did Management Say About 2026?

CEO Bouquard expressed confidence in the operating model: "Our fourth quarter loan originations of $927 million and loan repayments of $378 million continue to illustrate the velocity of our balance sheet and success of our investment and asset management strategy."

Post-quarter activity already includes:

- One new first mortgage loan: $81M commitment, $78.5M funded, Term SOFR + 2.65%

- One full repayment: $52.1M commitment, $49.5M UPB

The company also approved a new $25 million share repurchase authorization.

Key Risks to Monitor

- Office exposure — 10.6% of portfolio in challenged sector, though down from 17.8% YoY

- Rising leverage — Debt-to-equity at 3.02x, up from 2.14x at year-end 2024

- Declining liquidity — $143M down from $457.6M in Q1 2025 as capital deployed into originations

- Book value erosion — $11.07 vs $11.25 QoQ, driven by CECL provisions

- Interest rate sensitivity — A 100 bps decline in rates would reduce quarterly EPS by $0.02/share

Conference Call Details

The company will host a conference call Wednesday, February 18, 2026 at 9:00 AM ET.

- Dial-in: +1 (877) 407-9716 (US) or +1 (201) 493-6779 (International)

- Webcast: investors.tpgrefinance.com

Related Links: